NORTH AMERICA: Kansas City Southern has agreed to hold discussions with Canadian National over its unsolicited acquisition proposal, the railway announced on April 24.

After consulting the company’s legal and financial advisors, the board of directors had unanimously determined that the proposed cash and stock transaction valued by CN at US$325 per KCS share ‘could reasonably be expected to lead to a “Company Superior Proposal” as defined in KCS’s merger agreement with Canadian Pacific’ announced on March 21.

KCS therefore intended ‘to provide CN with non-public information and to engage in discussions and negotiations’ with respect to its proposal, ‘subject in each case to the requirements of the CP merger agreement’. However, KCS insisted that it ‘remains bound by the terms of the CP merger agreement’, adding that ‘there can be no assurance that the discussions with CN will result in a transaction’.

Responding to the announcement, CP said that it recognised that ‘the board of KCS is simply meeting its obligations under the merger agreement and fulfilling its fiduciary duty to its shareholders by assessing the CN offer. Not only is this the correct process and one that is clearly required by the merger agreement, in fact we are encouraged that they will be taking a hard look at the details of the CN offer as soon as possible, which we believe will lead them to question the true value and deal certainty of their proposal.’

In its initial response to the CN offer on April 20, CP described the rival proposal as ‘illusory and inferior because it creates adverse competitive impacts and raises other serious public interest concerns. CN’s proposal increases regulatory and anti-trust risk for KCS shareholders and decreases benefits for customers, employees and other stakeholders.’

‘We fully support the board of KCS in reviewing CN’s offer’, confirmed CP President & CEO Keith Creel on April 24. ‘We are confident through this process that they will recognise this unsolicited bid is fraught with challenges, uncertainties and regulatory risks that are not present in the seamless, pro-competitive and pro-service CP-KCS combination.’

Regulatory hurdles

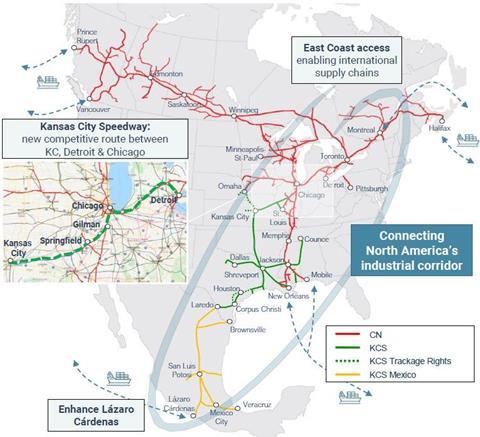

Asking whether the unsolicited bid was ‘real or just an attempt to thwart the agreement that KCS signed with Canadian Pacific’, CP questioned how CN planned ‘to get approval to create the third largest Class I railroad, with numerous overlapping connections across the US, when the Surface Transportation Board in 2001 purposely changed its merger rules to prohibit such anti-competitive deals?’

The Surface Transportation Board had confirmed on April 23 that the waiver from its revised merger rules granted to KCS in 2001 would be applicable to the proposed ‘friendly combination’ with CP.

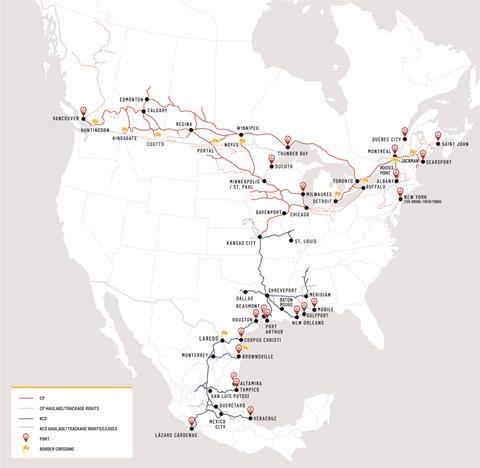

In its filing, the STB noted that ‘if approved, the combination of CP and KCS, the sixth largest and seventh largest Class I railroads respectively, would still result in the smallest Class I railroad, based on US operating revenues. In addition, a merger of the CP and KCS networks would appear to result in the fewest overlapping routes when compared to a merger between KCS and any other Class I carrier. The inter-relationship between the CP and KCS networks in fact appears to be end-to-end in nature, which likely raises fewer competitive concerns than a transaction that is not end-to-end.’

Welcoming the decision, CP said the two railroads would therefore ‘proceed with an application under the standards set forth in the STB’s pre-2001 major merger rules.’ It noted that ‘over 415 customers, ports, transloads and other stakeholders’ had already ‘filed letters with the STB supporting the combination’.

Acknowledging that the deal ‘remains subject to the approvals of CP and KCS shareholders and other customary closing conditions’, CP said it anticipated that the STB review would be completed ‘by the middle of 2022’, adding that the two railroads were looking forward to ‘an efficient, thorough and fair STB approval process’.

BofA Securities and Morgan Stanley are serving as financial advisors to KCS, while Wachtell, Lipton, Rosen & Katz, Baker & Miller, Davies Ward Phillips & Vineberg, WilmerHale, and White & Case are serving as legal counsel.