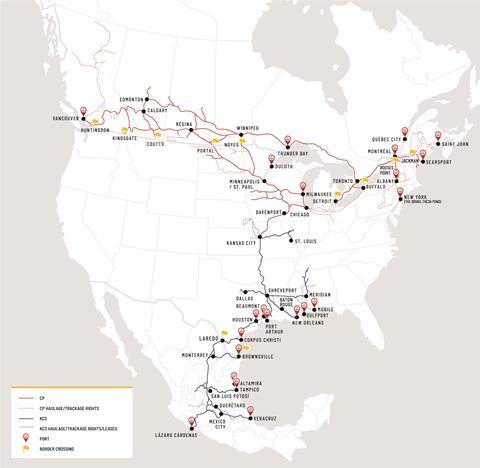

NORTH AMERICA: The two smallest Class I railroads, Canadian Pacific Railway and Kansas City Southern, have agreed to merge, creating what they say will be ‘the first US-Mexico-Canada rail network’.

Announcing the agreement on March 21, the two railroads said the deal ‘has the unanimous support of both boards of directors’. Subject to approval by the Surface Transportation Board and other regulatory authorities, the two railroads, which currently meet end-on at Kansas City, would combine to offer single-line service linking Canada, the northeast, midwest and south central regions of the USA, and much of Mexico.

To be known as Canadian Pacific Kansas City, the combined company would still be the smallest of the six remaining Class Is by revenue. Operating a network of 32 000 route-km with around 20 000 employees, the railroad would have annual revenues of approximately US$8·7bn.

According to the railroads, ‘seamless integration’ of the two networks would provide ‘dramatically expanded market reach’ and ‘new competitive transportation service options’ for their customers, which would support North American economic growth and create additional jobs across the combined network. They expect it to offer ‘meaningful environmental benefits’ in terms of driving modal shift from road, citing significant synergies ‘in the Dallas to Chicago corridor alone’.

Stock and cash transaction

CP has agreed to acquire KCS through a stock and cash transaction valued at approximately US$29bn, which includes the assumption of US$3·8bn of KCS debt. The shares would initially be placed in a voting trust pending regulatory approval of the merger. KCS common shareholders would receive 0·489 CP shares and US$90 in cash per share. This values KCS at US$275 per share, representing a 23% premium based on the CP and KCS closing prices on March 19. Following the merger, KCS common shareholders would own approximately 25% of CP’s outstanding common shares.

To facilitate the merger, CP plans to issue 44·5 million new shares. The cash portion of the transaction will be funded through a combination of cash-in-hand and the raising of approximately US$8·6bn in debt, for which financing has been committed. Together with the assumption of KCS debt, this would leave CP with an outstanding debt of approximately US$20·2bn.

Upon shareholder approval of the transaction, and the satisfaction of customary closing conditions, CP will acquire KCS shares and place them into a ‘plain vanilla’ voting trust, which would ‘insulate KCS from control by CP’ pending approval by the STB and ‘and other applicable regulatory authorities’. This step is currently expected to be completed in the second half of 2021, at which point KCS shareholders will receive their consideration.

While in the trust, the existing KCS management and board would continue to lead the company and pursue its independent business plan. The STB review of the transaction is expected to be completed by the middle of 2022, after which the two companies would be able to integrate their operations, ‘unlocking the benefits of the combination’.

The combination is expected to be accretive to CP’s adjusted diluted earnings per share the first full year, and to generate double-digit accretion upon the full realisation of synergies thereafter. ‘By accelerating the combined growth strategies of the two fastest-growing Class 1s with new efficiencies for customers and improved on-time performance under their respective PSR programmes, the combined company is expected to create annualised synergies of approximately US$780m over three years’, the railroads predicted.

Transformative integration

‘This transaction will be transformative for North America’, commented CP President & CEO Keith Creel, noting that ‘CP and KCS. have been the two best performing Class I railroads for the past three years on a revenue growth basis. The new competition we will inject into the North American transportation market cannot happen soon enough, as the new USMCA Trade Agreement among these three countries makes the efficient integration of the continent’s supply chains more important than ever before.’

‘KCS has long prided itself in being the most customer-friendly transportation provider in North America’, said KCS President & CEO Patrick Ottensmeyer. ‘Our companies’ cultures are aligned and rooted in the highest safety, service and performance standards. Customers, labour partners, and shareholders will all benefit from the inherent strengths of this combination, including attractive synergies and complementary routes.’

Following STB approval of the transaction, Creel is expected to become CEO of CPKC, and remain in post until at least 2026. Four KCS directors will join an expanded CP board. The combined entity will have its global headquarters in Calgary, with a US base in Kansas City and Mexico offices in Mexico City and Monterrey. CP’s current US headquarters in Minneapolis-St Paul will remain ‘an important base of operations’.